No Light Rail in Vancouver!

The Dog That Didn’t Bark

“Planning-

The federal government seized another big bank last week. Fannie Mae and Freddie Mac are on the verge of collapse and the fed is likely to announce a major bailout this week. More banks are expected to fail soon. “This is a very serious banking crisis,” says a former president of the American Bankers Association.

My suspicion is that government bailouts of the banks and lenders will only prolong

the agony. At least, that is what happened when Japan’s real-

While all kinds of reasons have been offered to explain the housing bubble, I still

insist that growth-

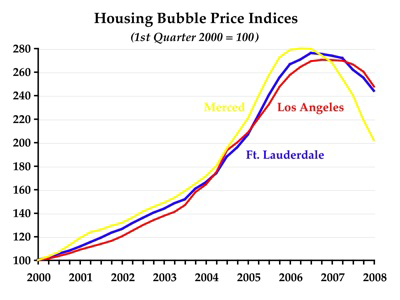

The figure above shows a classic bubble: steeply rising prices followed by a steep

fall that has yet to reach bottom. If you chart home price data from the Office of

Federal Housing Enterprise Oversight, you will find similar patterns throughout California,

Florida, Hawaii, Oregon, Washington, and other states with growth-

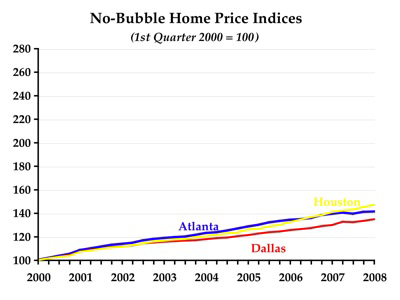

The dogs that didn’t bark are shown in the figure above: Atlanta, Dallas-

If no American cities had growth-

But because housing prices in California were rising with no end in sight, the money

that fled the telecommunications and dot-

So next time you fret about the devaluation of the dollar, the current recession, or even high fuel prices, thank an urban planner. They caused the housing bubble and they are responsible for the world’s current financial crisis.

34

Trackback • Posted in Planning Disasters

Reprinted from The Antiplanner

More on Housing

Some commenters on yesterday’s post want to pretend that the Antiplanner “cherry picked” three data series to show regions with a housing bubble and three more to show regions without a bubble. What rubbish.

My 2006 report on housing is based on data for 385 housing markets. Complete data are in the spreadsheet that I prepared for the report. You can use this spreadsheet to make your own charts like the ones in yesterday’s post for up to 6 metro areas at a time.

Of course, data in that report only go through 2005, so they show the bubbles but not the crashes. If you want more recent data, you can download them from the Office of Federal Housing Enterprise Oversight’s web site.

As I describe in my more recent Cato paper, the data reveal that most urban areas

that have done growth-

State growth-

The evidence shows that, if government does not stand in their way, home builders

can meet just about any demand for new housing. The three non-

Some commenters still hold the wishful belief that prices are higher on the coasts because the coasts are so much more desirable to live in than the interior. This does not explain why prices are so high in places like Boulder, which has been trying to manage growth for decades, but which is not near a coast. Prices are pretty reasonable in Colorado Springs, which has little growth control but is aesthetically at least as nice as Boulder. Meanwhile, many housing markets in North and South Carolina are very popular and near the coast, yet (with a few exceptions like Asheville and Charleston, both of which imposed various growth controls in the 1990s) did not experience bubbles.

It turns out that housing is an inelastic good. Like salt, we need it even if the price goes way up. What this means is that small restrictions on the supply of new housing can lead to large increases in price. And since sellers of existing homes are keenly aware of the price of new homes, if the price of new homes goes up, the price of all homes goes up.

Subprime mortgages, speculators, and Wall Street manipulations of mortgages all may have accelerated the recent housing bubble. But they did not cause it.

Without growth management, prices would not have been so high that lots of people

had to resort to subprime loans. Without growth management, rising prices would never

have attracted speculators to the market. Without growth management, the money that

fled the telecommunications and dot-

12

This was written the Following Day